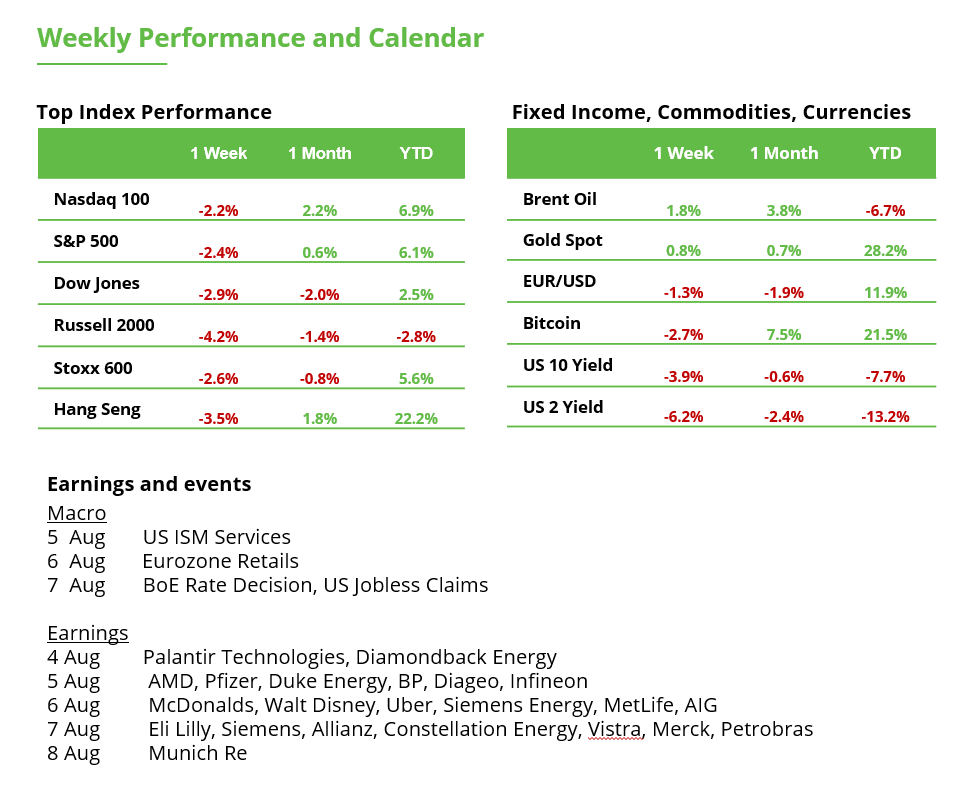

Analyst Weekly, August 4, 2025

Huge Tech feasts, the remainder nibble. Microsoft and Meta crushed Q2 earnings, however half of S&P 500 firms reported margin declines. Whereas buyers cheer AI-fueled progress, the true economic system’s displaying indicators of a tariff hangover and rising price complications.

Earnings Season: Energy on the High, Stress in Sure Pockets

The newest earnings season has underscored a widening divide in US fairness markets. On the prime, tech giants and massive banks have posted sturdy outcomes. Microsoft, Meta, JPMorgan, and Goldman Sachs all delivered double-digit revenue progress, reinforcing a notion of resilience in key segments of the index.

Beneath these headline beats, nevertheless, the story is extra nuanced. Current weeks have introduced tariff-related volatility, a weaker-than-expected jobs report, and softer earnings throughout client and cyclical sectors. Corporations like Ford and GM reported losses tied on to tariff prices. Supplies and industrial corporations additionally warned of margin compression. Oil majors Chevron and Exxon noticed earnings decline 31% and 23%, respectively, whilst they maintained buybacks and dividends.

Throughout the S&P 500, income progress stays optimistic, however earnings are underneath pressure, particularly in sectors tied to the true economic system corresponding to vitality, supplies, and industrials. Eight of 11 sectors reported year-over-year declines in internet revenue margins in Q2 2025. Regardless of this broad trailing weak point, index-level earnings forecasts stay unfiltered, due to sturdy margin efficiency in know-how, monetary, and communication companies.

What we’re seeing then, shouldn’t be uniformly broad-based energy, however relatively a market the place sturdy efficiency from a small variety of mega-cap shares continues to form the headline narrative, successfully muting the underlying softness in additional cyclically delicate components of the economic system.

Supply: Bloomberg, as of July 31, 2025.

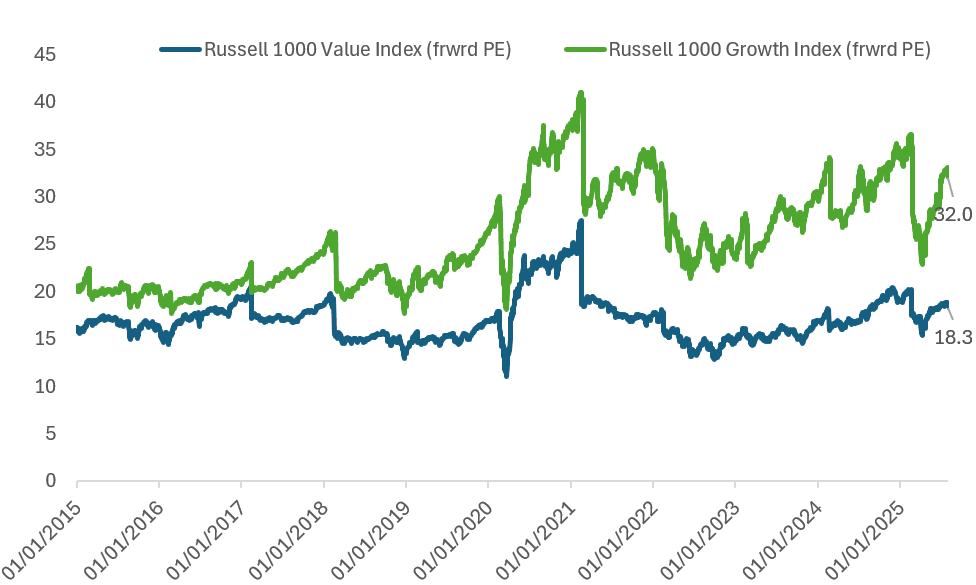

Why the S&P 500’s Valuation Doesn’t Inform the Complete Story

Regardless of indicators of weak point throughout massive components of the index, the S&P 500 continues to commerce at ~22–24x ahead earnings. Progress-oriented shares commerce close to 32x, whereas worth names stay nearer to 18x, highlighting a widening disconnect in how future earnings are being valued. That is as a result of outperformance of a slender set of extremely capitalized, tech-driven corporations whose management now disproportionately shapes index-level valuations.

This focus is seen in sector weights too. NVIDIA alone now accounts for 7.7% of the index, on its solution to equaling all the healthcare sector at 9.0%. Conventional defensive sectors corresponding to utilities (2.4%), staples (6.0%), and healthcare (9.0%) have fallen to their lowest mixed index share (17.4%) in over twenty years.

Historically, buyers turned to those defensive fairness sectors in addition to long-duration Treasuries to hedge draw back dangers. However with defensive sectors out-weighed by Magazine 7 names and bonds nonetheless underwater almost 10 months after the primary fee minimize, these hedges have confirmed ineffective.

Consequently, investor curiosity has shifted towards extra constant draw back safety and valuation help, together with:

Actual belongings, commodities and infrastructure performs

Uncorrelated diversifiers, together with digital belongings and gold

Multi-asset earnings methods

Regional and worldwide worth performs

Throughout each theUS and worldwide markets, there are pockets of firms buying and selling at 6–10x normalized earnings, typically with stability sheet energy and free money movement yields properly above market averages. In sectors like vitality, regional banking, and industrial manufacturing, valuations have compressed regardless of steady or enhancing operational efficiency. Many of those companies are priced close to or beneath guide worth, with dividend protection supported by working money flows relatively than progress projections.

In a market more and more pushed by momentum and concentrated progress narratives, these missed segments provide a extra grounded path, not essentially as contrarian bets, however as a part of a extra balanced, valuation-aware method to portfolio development.

Supply: Bloomberg, as of August 3, 2025.

Conclusion: Recalibrating Valuation Consciousness

The S&P 500’s energy is being pushed by a small group of sectors, primarily tech and financials, boosted by AI-related spending and funding. However underneath the floor, many components of the true economic system, like autos, airways, and client items, are seeing shrinking margins, and extra unsure earnings. On this context, the index’s headline a number of now not displays the typical underlying enterprise.

For buyers reconsidering how they construct their portfolios, it could make sense to concentrate on methods which might be diversified, valuation-aware, and grounded in fundamentals like regular earnings, strong stability sheets, and the flexibility to carry up in harder situations.

Comeback of the Buck?

The U.S. Greenback Index ended final week with a achieve of 1.0%, closing at 96.68. At its peak through the week, the greenback was up as a lot as 2.6%. Nonetheless, Friday’s lengthy purple candlestick, within the type of a bearish engulfing sample, signifies that merchants have not too long ago pulled again from the greenback within the quick time period.

Within the medium time period, the breakout above the June 23 excessive at 98.96 could have marked the start of a brand new upward pattern. If the rally continues, the decrease highs from this 12 months’s earlier downtrend may function potential upside targets: 100.05 and 101.52. Additional above, the long-term 200-day transferring common is situated at 102.91.

The 50-day transferring common may act as key help in case of a deeper pullback. Then again, a decisive break beneath it may carry the current low at 96.67 and the July low at 95.91 again into focus.

U.S. Greenback Index within the every day chart

Key Week for German Q2 Earnings

Infineon: A semiconductor producer enjoying a key position within the vitality transition, digitalization, and e-mobility. Nonetheless, competitors is intense. Market chief TSMC, the producer of Nvidia chips, is adopted by U.S. giants corresponding to Broadcom, AMD, and Qualcomm, in addition to European heavyweights like ASML. Infineon stays closely depending on the automotive sector. With regard to U.S. tariffs, it is going to be notably attention-grabbing to see on Tuesday how the corporate plans to strategically place itself going ahead. The inventory prolonged its losses by 1.8% final week and is at present in a correction part.

Siemens Vitality: International vitality demand is predicted to rise considerably within the coming years attributable to e-mobility and the AI increase. Siemens Vitality is properly positioned to play a key position right here. Strategically, the corporate holds important applied sciences wanted to help the technical aspect of the vitality transition. Buyers ought to watch carefully on Wednesday how Siemens Vitality manages its tasks within the U.S. The corporate plans to start out producing massive industrial energy transformers within the U.S. by 2027. Siemens Vitality is the third-best DAX performer year-to-date, with the share worth almost doubling. Simply final week, it reached a brand new file excessive.

Rheinmetall: Rheinmetall is considerably extra extremely valued than most of its defense-sector friends. This will increase the strain to ship sturdy earnings. As well as, the current commerce deal between the U.S. and the EU may drawback European protection firms, as billions in EU protection budgets are anticipated to shift towards U.S. merchandise. Regardless of these dangers, the protection increase stays intact. Structural demand continues to help the trade. On Thursday, buyers ought to focus particularly on Rheinmetall’s strategic course, order consumption, and any steering revisions. The inventory is at present holding above a key help degree.

Rheinmetall within the weekly chart

Different DAX firms reporting this week:

Siemens (Thursday): Trade and automation know-how

Deutsche Telekom (Thursday): Telecommunications and IT companies

Allianz (Thursday): Insurance coverage and asset administration

Munich Re (Friday): Reinsurance and danger administration

This communication is for info and schooling functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding goals or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}