Please see this week’s market overview from eToro’s world analyst staff, which incorporates the newest market knowledge and the home funding view.

Dangerous belongings up globally for a powerful end of Q3

US GDP development for Q3 was confirmed at 3.0%, and softer Private Consumption Expenditure (PCE) inflation knowledge for August, at 2.2%, supported the Federal Reserve’s outlook for a “Goldilocks” situation. This optimism helped the S&P 500 and Dow Jones shut the week up by 0.6%, whereas the Nasdaq rose by 1.1%. The European STOXX gained 2.7%, and Japan’s Nikkei added 5.6%. Nonetheless, probably the most exceptional efficiency got here from Hong Kong’s Cling Seng, which surged by 13%, its greatest week in 16 years, highlighting a rotation in direction of areas beforehand lagging the US.

As of the top of Q3, the S&P 500 is up 20% for the yr, Nasdaq +19%, Cling Seng +21%, gold +28%, and Bitcoin +54%, providing sturdy returns throughout varied funding methods. With This fall historically performing nicely, optimism stays excessive for the rest of 2024.

China’s $284 billion stimulus bundle

Reduction for Chinese language equities arrived when the Chinese language authorities unveiled a big financial stimulus bundle to handle the slowing economic system and stabilise the property market. The PBoC lowered rates of interest, lowered reserve necessities for banks, and launched measures to decrease mortgage prices, benefiting 50 million households. Moreover, the bundle included new insurance policies geared toward bolstering the inventory market and issuing 2 trillion yuan in bonds to assist native governments and stimulate shopper spending.

Outlook October

October will shift the main focus again from macro to micro, with JP Morgan unofficially kicking off the brand new earnings season on October 11, operating by means of to NVIDIA’s report in mid-November. Analyst expectations for realised income and earnings development in Q3 stay modest however are considerably larger for the following durations. As time goes on, investor consideration will more and more flip to the end result of the tense US presidential election on November 5, in addition to the high-profile BRICS Summit in Russia, starting on October 22. For extra steerage, watch our This fall Funding Outlook video resulting from be launched on October 7.

The US labour market should not cool a lot additional

The US labour market knowledge for September, due for launch on Friday, is of paramount significance to traders. The Federal Reserve has made it clear that its precedence is to keep away from additional cooling of the labour market, as reaching a “comfortable touchdown” stays its prime aim. Any indicators of weak point within the labour market might improve the possibilities of the Fed contemplating a further 50 foundation level charge reduce in November. Nonetheless, such indicators can also set off heightened volatility within the markets. A reasonable improve of 145,000 new jobs is anticipated, whereas the unemployment charge is anticipated to stay regular at 4.2%.

Rate of interest cuts not but adequate for property increase

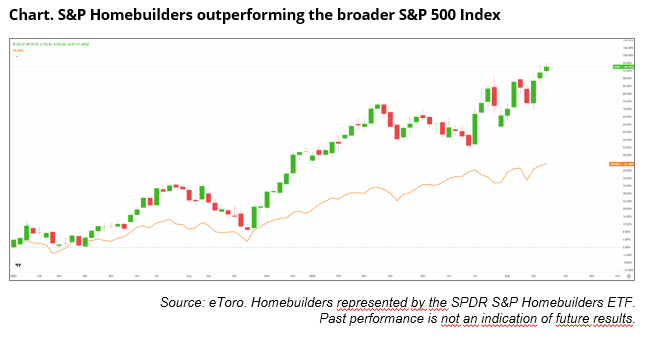

The US homebuilder sector has considerably diverged from the S&P 500 since late 2023 (see chart beneath), as traders anticipate the constructive influence of forthcoming charge cuts on the housing market. The SPDR S&P Homebuilders ETF has delivered greater than double the return of the broader market for the reason that begin of 2023. Regardless of this optimism, a full restoration in the actual property sector has but to materialise, as weak constructing allow and housing begin figures counsel. Though there have been occasional sturdy months, a sustained upward pattern stays elusive. The 30-year mounted mortgage charge has dropped to six.1%, making homebuilding extra reasonably priced, however for a real increase, charges would want to fall additional. The normalisation of financial coverage is on the horizon.

Earnings and occasions

Earnings are due for Nike (the place Elliot Hill will substitute John Donahue as CEO), Carnival Cruise Traces, Levi Strauss and Constellation Manufacturers. Buyers will likely be watching not solely Chinese language shares comparable to Alibaba, Tencent, JD.com, PDD, BYD and NIO after the historic rally following the financial stimulus announcement final week, but in addition luxurious items makers comparable to LVMH, Tesla and Apple with a powerful deal with the Chinese language shopper.

Wanting forward on the agenda, subsequent week we’ll see Amazon Prime Massive Deal Days (Oct.8-9), TSMC month-to-month gross sales (Oct.9), Tesla robotaxi unveil (Oct.10), and JP Morgans Q3 earnings (Oct.11), marking the unofficial begin of the brand new earnings season.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out considering any explicit recipient’s funding aims or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product will not be, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}