With 37 completely different manufacturers and 4 divisions, Loreal ($OR.PA) has been on my radar since I began investing. But it surely has by no means been at a reduction. Right this moment, buying and selling at 30x PE, it’s a kind of high-performing firms that not often disappoint. Is it price investing now, or ought to we anticipate a greater alternative?

Supply: L’Oréal F2024 Annual Report.

Key Highlights

A Magnificence Big at 30x PE – L’Oréal has dominated for over a century, however is it nonetheless a purchase at this valuation?

AI-Pushed Edge – With 694 patents in 2024, tech innovation fuels development. Will it maintain premium pricing?

Progress vs. Stagnation – Enlargement slows, inflation bites. Is L’Oréal nearing its limits?

Enterprise overview

In 1909, a scientist in Paris developed one thing by no means seen earlier than: a safe-to-use hair dye, marking the start of L’oréal with Eugène Schueller. The long-lasting “As a result of I’m worthy” was the primary commercial of the model in 1970, however it’s nonetheless related at this time.

The sweetness business has proven resilience even within the worst disaster worldwide, and might discover the explanations behind this by searching for the “lipstick impact,” an actual financial principle explaining why customers proceed spending on inexpensive luxuries.

Supply: L’Oréal.com.

Supply: L’Oréal.com.

Magnificence markets are rising in the direction of the course of not solely feminine, however a extra inclusive sector, the place males, the aged, and even children are utilizing magnificence merchandise, which will increase the business’s attain.

L’Oréal has been one of many firms that higher perceive the worth of AI of their processes, as they stated:

“We’ve got optimized the work of our workers, giving them extra time for greater value-added duties, corresponding to growing methods via information evaluation, danger administration, and anticipation.” – L’Oreal investor presentation.

Their CEO, Nicolas Hieronimus, is the instance of management we search for in firm administration, working within the firm since 1987, began as a product supervisor and climbed as much as develop into the CEO in 2021. We would like within the administration of our companies dedication, beliefs in the way forward for the corporate, and particularly deep data in how your organization works, processes, and generates revenues.

34.7% of the shares of the corporate are owned by the Betancourt household, and they’re a part of the board of administrators the board, guaranteeing their sturdy private dedication to the corporate’s long-term imaginative and prescient.

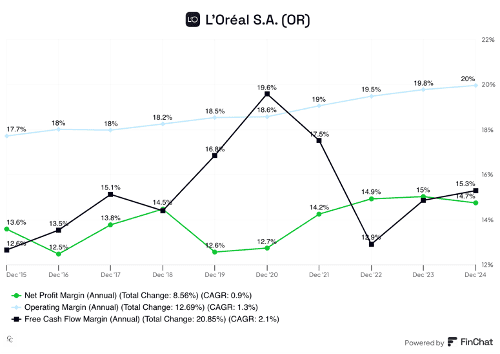

Monetary evaluation

After we speak about monetary well being, L’Oréal should be one of many firms with higher historic efficiency I’ve seen. Common income development of 6,99%, with a powerful historic capital effectivity with a Return on Capital Employed from 17% to 25%.

The worldwide magnificence market worth is about 290$ Bn, rising 4,5% yearly. By 2030, estimations are that 60% of the inhabitants will devour magnificence merchandise, which might imply 750 million extra folks shopping for magnificence merchandise.

Supply: Finchat.

Nonetheless, as a holding firm with a number of manufacturers below its umbrella, L’Oréal’s complexity makes it troublesome to evaluate the detailed efficiency of every enterprise phase. This construction can generally obscure underlying points, and I stay cautious about assuming steady, uninterrupted development in income, margins, and web earnings.

Pessimistic Situation: We thought-about a 20x P/FCF a number of with attainable stagnation in gross sales, factoring within the dangers of a significant disaster within the coming years that might affect anticipated development. This ends in a -22.92% lower within the funding worth.

Base Situation: We raised the a number of to 25x, accounting for some development. Nonetheless, at present costs, we might nonetheless see a -5.37% lower in funding worth.

Optimistic Situation: Solely on this case would we notice positive aspects, assuming a 28x a number of and the expansion L’Oréal expects over the subsequent three years. 28x is the a number of I assign to high-gain companies with aggressive benefits and powerful development expectations.

As a result of we solely make investments if we received’t lose cash below any situation, L’Oréal doesn’t appear to be a horny funding at these costs. Our objective retains being the identical: “Don’t lose cash.”

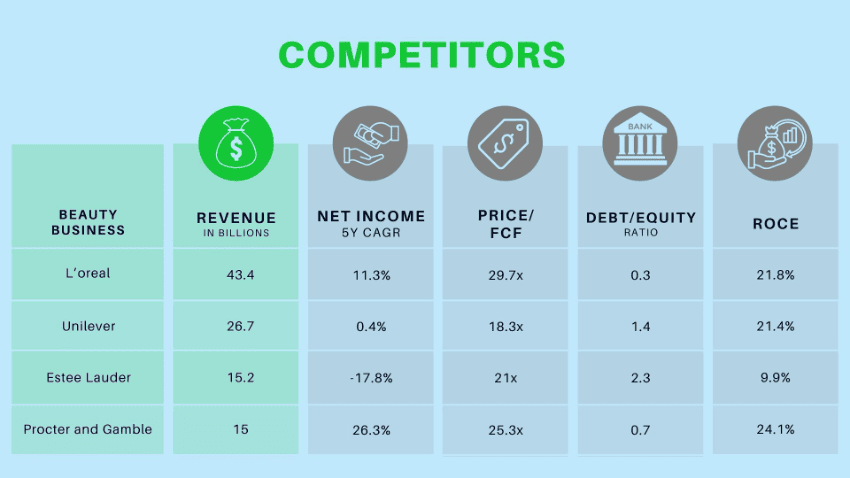

Comparative

Supply: Finchat.

Amongst all magnificence firms, L’Oréal is the most important by way of market share. In comparison with Unilever and P&G, its income is solely derived from the sweetness phase.

One key aggressive benefit is L’Oréal’s resilience in Asia. Whereas the corporate reported a 3.2% decline in This fall gross sales, Estée Lauder skilled a a lot sharper 11% decline in the identical interval.

L’Oréal continues to steer in innovation, submitting 694 patents in 2024 and investing €1.3 billion (3% of gross sales) in analysis and innovation.

Their AI-powered digital magnificence assistant, Magnificence Genius, has supplied personalised diagnostics and proposals to over 100,000 customers in 2024.

BETiq improves advertising and marketing effectivity and return on funding. At the moment applied in 6 international locations, it’s anticipated to increase to eight by 2025.

CreAItech makes use of AI-powered creativity to boost content material creation.

L’Oréal pays a 2.05% dividend, with a 6% enhance in 2024, marking the best dividend development in 10 years. The corporate additionally accomplished €0.5 billion in share buybacks.

Dangers

Stagnation Threat – As L’Oréal reaches world saturation, future development might develop into tougher. Enlargement into Africa and Asia would require greater investments and elevated operational prices.

Asian Competitors – The sweetness market in Asia is extremely aggressive, making it troublesome for L’Oréal to seize extra market share.

Inflation & Forex Dangers – Presence in high-inflation international locations like Argentina and Turkey poses dangers, although some prices are offset by the latest power of the Euro.

Political Dangers – Trump’s potential tariffs on imports might cut back L’Oréal’s margins within the essential U.S. market.

Retailer Dangers – Gross sales in pharmacies and drugstores have slowed as a consequence of declining foot site visitors, affecting total efficiency.

Enlargement Dangers – Shifting into dietary supplements requires vital CAPEX funding, and an absence of expertise on this phase poses execution dangers

Conclusion

I don’t suppose we are going to ever see L’Oréal at considerably decrease valuations. Nonetheless, as a consequence of its dimension, it can finally attain a degree the place its unbelievable sustainable development will decelerate. We are able to justify paying a premium for high-quality companies, however a valuation of 25-28x PE appears acceptable.

Progress expectations for 2025 are 4-4.5%, indicating stabilization fairly than overperformance. At present valuations, I’m not shopping for, however I’ll monitor for a worth drop. Nonetheless, for dividend-focused traders in search of a dependable blue-chip inventory, L’Oréal stays a horny selection.

This communication is for info and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding targets or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product aren’t, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}